© rawpixel/Getty Images

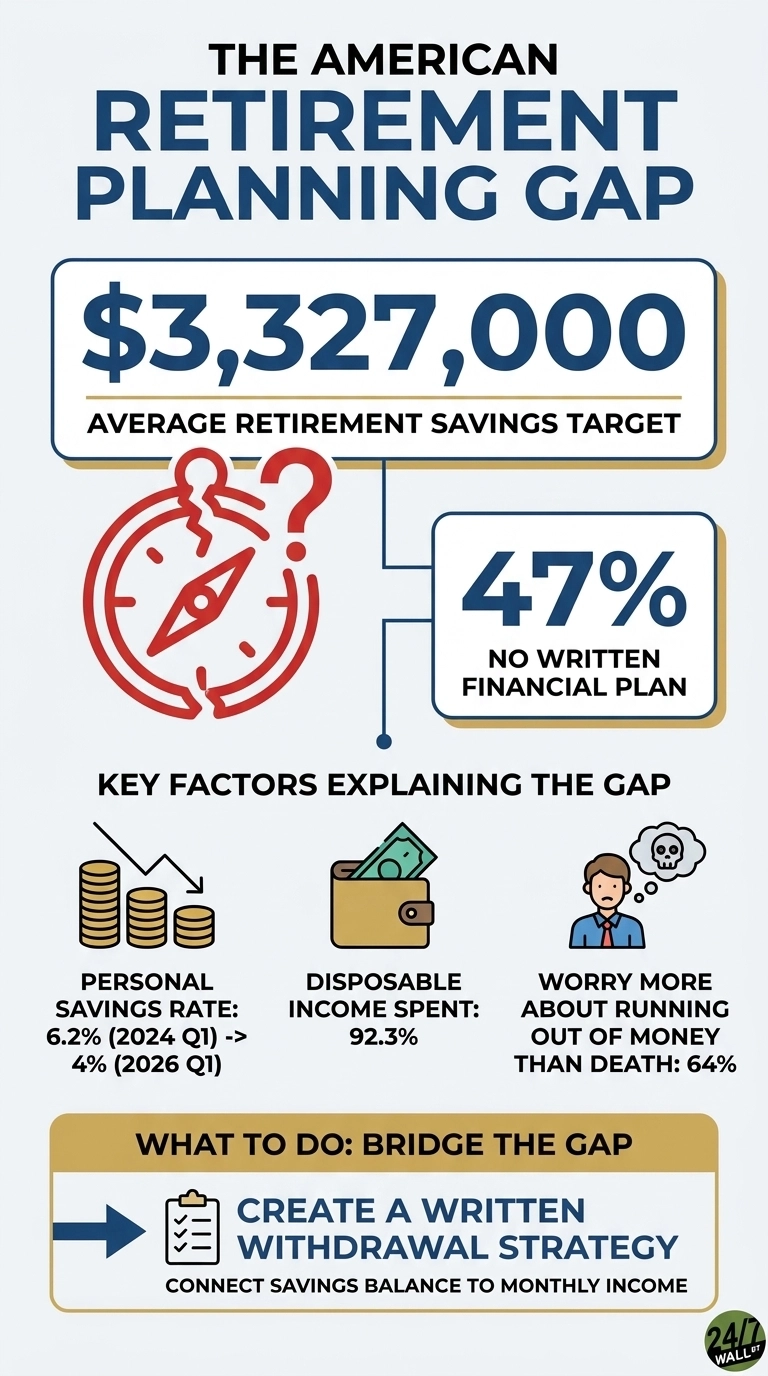

Nearly half of Americans are saving without a roadmap, and a Recent Allianz Study has put a sharp number on their costs. According to the study, 47% of Americans do not have a written financial plan, and only 45% know how they will turn their savings into income in retirement. The accumulation phase is going well in many households, but it is the conversion phase, where the balance becomes salary, is where things fall apart.

The title difference here is pretty straightforward, for better or worse. Americans who have set a retirement goal are aiming for an average of $3,327,000 to retire comfortably. At the same time, 45% do not know how much they actually need to save. The $3.3 million number floating in someone’s mind without any exit strategy is the same as a wish with a dollar sign in front of it.

24/7 Wall St.

24/7 Wall St.

Difference between balance and planning

A written financial plan is a document that combines three things: what you have, what you will need each year in retirement, and the order in which you will draw accounts to produce that income. Without it, a 401(k) balance is just a number on a statement. Allianz’s finding that 59% of Americans admit they don’t know what else they should do to prepare reflects the problem. People are contributing to accounts and watching the balances grow, but they can’t answer the next question: How do those dollars become a monthly check that lasts 25 or 30 years?

This uncertainty is visible in how people feel. Confidence in being able to financially support a desired lifestyle has declined 13% since 2020, and 64% of Americans now say they are more worried about running out of money than dying. Concern about Social Security has increased in parallel, with 67% expecting it will not last until their retirement, up from 57% in 2024.

macro backdrop not helping

Allianz study shows Americans want to leave something behind – 51% say they would prefer to leave a financial legacy rather than spend everything during retirement: “More than half of Americans (51%) say they would like to leave a financial legacy…” Young adults in particular are thinking early about inheritance, even as they grapple with low self-confidence and competing financial pressures. The report says 62% of Americans feel pulled in too many financial directions, and 59% say they don’t know what else they should do to prepare for retirement.

Whether that initial intention becomes actual inherited property depends on three concrete steps: make a will, Naming beneficiaries on each retirement and insurance accountAnd saving at a level that leaves something behind. The survey clearly reflects the aspiration. Implementation is still uncertain.

What Americans say they want

The same study makes the demand side unusually clear, as 74% of Americans would prefer to adopt financial products that protect against large losses, even if it means giving up large gains, and 92% say a product offering guaranteed income in retirement would help them support the life they want. Hunger is one of predictability, a kind of written plan with a defined withdrawal sequence that is designed to be delivered.

What the data really shows

Allianz’s findings point to a structural gap that appears even among households that actively contribute to retirement accounts. Americans are saving in an environment where 47% don’t have a written financial plan and 59% say they don’t know what else they should do to prepare for retirement, lines taken directly from the study: “Nearly half of Americans (47%) do not have a written financial plan…59% admit they don’t know what else they should do to prepare for retirement.” The labor market may be stable, and wages rising nationally, but the story of the survey is not about macro conditions; It’s about the missing bridge between a balance and a reliable income stream.

The bridge, the part of a retirement plan that requires a written withdrawal strategy, is a Social Security Claim DecisionAnd tax indexing, is the piece that most homes haven’t made. Allianz documents that only 45% of Americans know how they will convert their savings into income, and 53% believe that just having a retirement account will be enough. The difference becomes even more stark when paired with the study’s savings goals: Of Americans who have a number in mind, they say they need $3,327,000 to retire comfortably, but nearly half have no plan to convert that number into monthly income.

The study puts a number on the paradox. People are saving, but without a plan to convert that savings into a sustainable income stream, the costs show up later, when the balance has to start paying the bills.