Procter & Gamble (PG +2.67%) has just announced its 70th consecutive annual dividend increase, increasing its quarterly payout from $1.0568 per share to $1.0885 per share or $4.354 per year – good for a forward yield of 3% based on the share price at the time of this writing.

Dividend increase makes P&G one of the longest-tenured stocks dividend kingWhich are companies that have increased their payout for at least 50 consecutive years. There are 57 dividend kings – but only five of them have increased their dividends for at least 70 consecutive years.

This is why P&G is the top dividend payer value stock To buy now.

Image Source: Getty Images.

P&G is in a league of its own

Procter & Gamble is the world’s largest home and personal products company Third largest US consumer staples company by market cap — Back wal-mart And costco wholesalebut further coca cola.

P&G has a portfolio of leading brands across everyday use categories:

- Diapers (led by Pampers)

- paper towels (reward)

- Toilet Paper (Charmin)

- Tissues (Puffs)

- Feminine Products (Forever Led)

- Grooming and hair care (Gillette, Old Spice, Pantene, and Head & Shoulders, among others)

- Cleaning products (Dawn, Cascade, Febreze, etc.)

- Laundry detergent (Tide, Gain, and others)

- Oral and personal health care products (Crest, Oral-B, Vicks, etc.)

- Skin & Personal Care (Olay, SK-II, etc.)

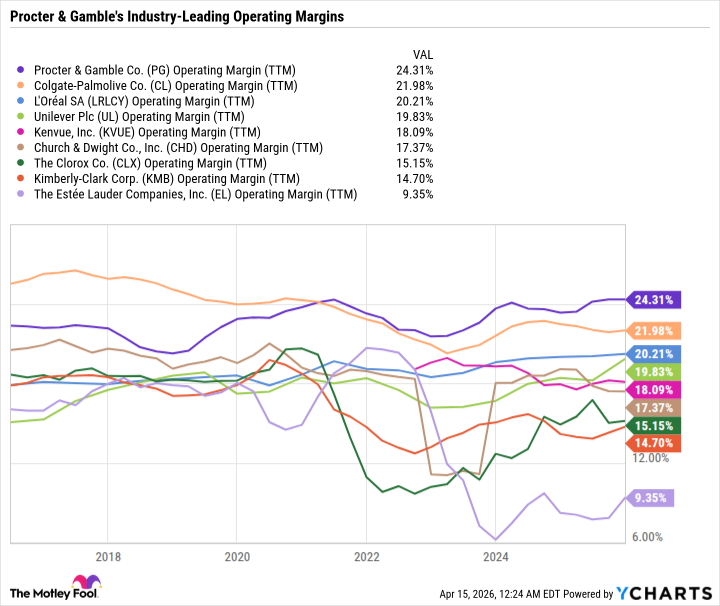

P&G’s international brand recognition, distinctive supply chain and marketing, and sheer size across all categories provide it with impeccable pricing power and negotiating leverage with retailers. These advantages allow P&G to consistently generate operating margins above 20% – often ahead of its peers.

PG Operating Margin (TTM) by data YCharts

Despite its competitive advantage, P&G’s growth has slowed in recent years due to consumer spending challenges driven by higher living costs and inflationary pressures, including higher everyday spending and now increased oil prices. P&G is generally considered a recession-proof business because demand for its products remains consistent throughout economic cycles. But when budgets are strained, consumers may change their behavior and make choices Buy a private-label brand like Costco’s Kirkland Signature DiapersFor example, to stretch your dollars instead of Pampers.

today’s change

(2.67%) $3.82

current price

$146.93

key data points

market cap

$341B

day limit

$143.16 -$147.59

52wk range

$137.62 -$170.99

volume

11m

average volume

11m

gross margin

51.11%

dividend yield

2.88%

a measured dividend increase

Considering P&G’s business situation and Slowdown in the broader household and personal products industryIt’s not surprising that P&G’s latest dividend increase was only a 3% increase. Historically, it is far more common to see P&G raise its dividend in the mid to high single digits. But it’s not unheard of for P&G to announce low-single-digit growth.

The most recent example was 2023, when P&G coincidentally also raised its dividend by just 3%. It made sense at the time, given that P&G was coming off years of price hikes and inflation pressures were rising after the pandemic.

Maintaining a 70-year streak of dividend increases means P&G must consistently grow its earnings and avoid excessive growth, especially during good years, because the last thing P&G wants is for the dividend expense to grow so large that it swallows up all of its free cash flow (FCF).

P&G’s dividend expense is still at a good level. Its trailing 12-month earnings of $6.75 and FCF per share of $6.09 easily cover its dividend even after the latest increase. And the payout ratio of 61.9% is pretty solid for a consumer staples company.

P&G is a uniquely resilient group

Besides high margins, earnings and FCF, what makes P&G such a distinctive dividend stock is its ability to take what the market gives by leaning into whatever product categories and geographies are performing well.

For example, in P&G’s latest quarter, which was the second quarter of fiscal 2026, Latin America and Europe helped offset the weak performance in North America. Hair care was P&G’s best-selling category, and skin and personal care, personal health care, home care and oral care also helped offset weak performances in beauty, clothing care, baby care, feminine care and daily care.

P&G is not heavily dependent on any particular region or product category. And even within specific categories, it can maintain customer sales even during a reduction in spending. For example, a customer may turn to a generally less expensive detergent brand such as Tide from Gen or Pampers from Luvs to cut costs. But P&G still lands sales because it has both premium-priced range options and more budget-friendly options.

A Top Stock to Buy and Hold

P&G is one of the most reliable dividend stocks for value investors to buy and hold. But P&G rarely trades at a discount S&P 500 (^GSPC +1.20%)Considering its quality.

Now there is an incredible opportunity for investors to buy P&G on the sale. The selloff in the stock has pushed its yield to a nearly five-year high and valuation to a five-year low. P&G has a price-to-earnings (P/E) ratio of only 21.4 and a forward P/E of 20.8, compared to 20.3 for the S&P 500.

Add it all up, and P&G checks all the boxes for a dividend stock that can anchor a passive income portfolio.