last summer, clorox (clx +2.33%) raised its quarterly dividend to $1.24 per share, the 48th consecutive annual dividend increase. This puts Clorox on track to reach the coveted 50-year dividend streak milestone and join the list of fewer than 60 other companies that can appropriately be called dividend king.

Clorox’s aspirational royal status, combined with its huge 5.7% dividend yield, makes it a no-brainer buy for passive income. But Clorox has a lot of work to do if it wants to regain and maintain its status as the dividend king.

Clorox can be unreliable value stock For patient investors, but there are some red flags that are worth considering before buying.

Image Source: Getty Images.

Not all dividends stay on the king’s throne

To consistently grow its dividend year after year, a company must grow its earnings and free cash flow (FCF). If earnings growth stops or falls, the dividend will eventually become unaffordable, and the company will have to either stop raising its payout or cut the dividend.

3M (mmm 1.90%) This is the latest example of a former dividend king that cut its payout in 2024. The decision to do so proved to be the right one, as 3M freed up much-needed cash to turn the business around, and the stock has rebounded accordingly. In comparison, coca cola (To 1.01%) is about As reliable a dividend king as you can getThanks to its distinctive brand identity, global exposure, high margins from an efficient supply chain and consistent demand regardless of the market cycle.

Despite falling earnings and FCF, Clorox has continued to grow its dividend – making it more like 3M before the dividend cut than staid giants like Coca-Cola. In the nine months ending March 31, 2026, Clorox paid $452 million in dividends, but generated only $161 million in FCF. When adjusting for the outright $476 million purchase of a larger interest in its Glad Bags and Wraps business, Clorox generated $637 billion in FCF, which easily covers the dividend. Similarly, adjusted earnings per share of $1.64 outweighs the $1.24 dividend payment.

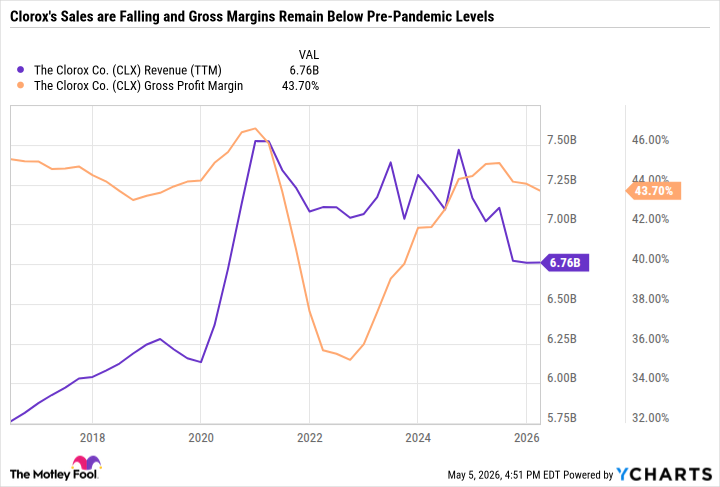

But as you can see in the following chart, Clorox’s sales are declining (partially due to divestitures), and the direction of its margin improvement has reversed.

CLX Revenue (TTM) by data YCharts.

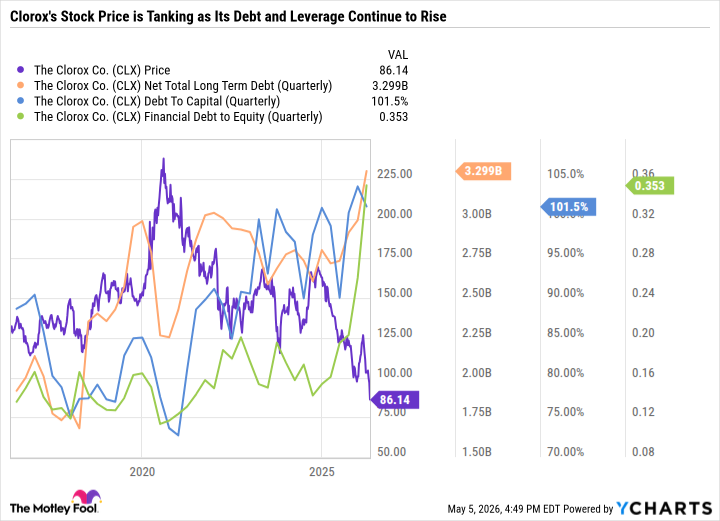

Although margins have recovered from their lows, they are still below pre-pandemic levels. Meanwhile, Clorox’s balance sheet is in the worst shape in a decade, as net long-term debt and leverage ratios have skyrocketed – in line with its falling stock price.

An unstable regime is forming

Clorox is doing well with its cost-cutting efforts, such as lower advertising investments and selling and administrative expenses to offset higher manufacturing and logistics costs. In February, Clorox completed its five-year, $580 million transition to a new enterprise resource planning system to increase efficiency. Those efforts are a step in the right direction to make Clorox a better-run company. But ultimately, its long-term growth depends on how its brands connect with consumers, and whether they are differentiated enough to maintain pricing power despite competition from other name brands and private label.

today’s change

(2.33%) $2.10

current price

$92.11

key data points

market cap

$11B

day limit

$89.90 -$93.45

52wk range

$84.70 -$138.94

volume

3.9M

average volume

2.6

gross margin

43.70%

dividend yield

5.51%

At just 15.7 times forward earnings, value investors who are confident in the sustainability strength of Clorox’s brands may want to buy the stock. However, Clorox has a long way to go to regain the credibility of a rock-solid stock like Coca-Cola, even if it could technically become a dividend king over the next 15 months.