benchmark S&P 500 The index has had a rough start to 2026 and has lost about 5% of its peak value. As geopolitical tensions and economic uncertainty increase, this selloff could turn into a correction of 10% or more. But throughout history, the S&P 500 has always reached new record highs over a longer period of time, so declines usually represent buying opportunities for investors.

For this reason, I bought C Ltd (SE 4.13%) Stock earlier this month. It is a Singapore-based technology powerhouse that operates three core businesses in the e-commerce, gaming and digital financial services sectors. Its stock has recently been hit hard by the market, falling 56% from its 52-week high.

But I think it’s a solid buy based on its extremely attractive valuation and the company’s rapid financial growth.

Image Source: Getty Images.

Triple threat in digital economy

C owns Shopee, the largest e-commerce Forum in Southeast Asia. It processed 13.9 billion orders worth $127.4 billion during 2025, and both numbers were at record highs. C has been squeezing more revenue out of Shopee over time by selling digital advertising on the platform. It is also improving its logistics network to deliver products to customers more quickly, resulting in more orders.

today’s change

(-4.13%) $-3.49

current price

$80.98

key data points

market cap

$46B

day limit

$79.89 -$82.20

52wk range

$77.05 -$199.30

volume

5.3M

average volume

5.9M

gross margin

45.84%

Then there’s C’s digital financial services platform, Moni. It lends money to Shopee merchants to help them grow their businesses, and it also offers Buy Now, Pay Later Loans to consumers to increase their purchasing power. Moni had 37 million active borrowers at the end of 2025, an increase of 40% year-on-year. They had $9.2 billion in debt, more than 80% of which was delinquent.

C’s third and final business segment is digital entertainment, which is home to the company’s Garena. game development studio. Garena is responsible for some of the world’s most popular mobile games, including free fire, Call of Duty: MobileAnd ea sports fc. The studio served more than 633 million users during the fourth quarter of 2025, a slight increase compared to the same period in 2024.

C’s revenue growth is accelerating

C to generate a record $22.9 billion in total revenues through 2025, representing an increase of 36.4% year-on-year. Growth accelerated for the second year in a row, highlighting the company’s incredible momentum. Here’s how its 2025 revenue breaks down.

|

Section |

2025 revenue |

year-on-year growth |

|---|---|---|

|

E-Commerce (Shopee) |

$16.6 billion |

33.4% |

|

Digital Financial Services (Money) |

$3.8 billion |

60.1% |

|

Digital Entertainment (Garena) |

$2.4 billion |

26.1% |

Data Source: C Ltd.

Although the e-commerce business is clearly C’s largest source of revenue, it operates at very low profit margins as it aims to offer customers the lowest possible prices. But it made progress in 2025, with $880.6 million in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA), C’s preferred measure of profitability. This is 465% more than in 2024.

That said, the digital financial services and digital entertainment segments produced a combined $2.7 billion in adjusted EBITDA for the year. Enough Less revenue. That’s the advantage of managing such a diverse group of businesses.

Overall, even on the basis of Generally Accepted Accounting Principles (GAAP), C had a low year. The company delivered net income of $1.6 billion, up 259% from 2024.

Marine stocks look cheap right now

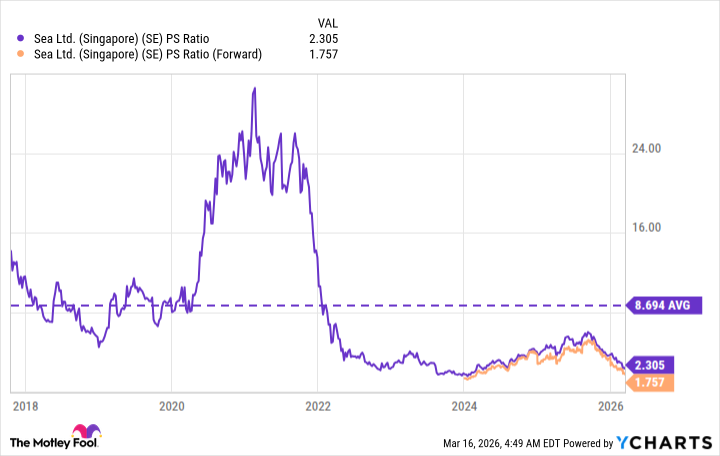

After a 56% decline from its 52-week high, C stock is trading at very attractive valuations. Its Price-to-Sales (P/S) Ratio is only 2.3, which is a Important That’s a discount to its long-term average of 8.7, when the stock went public in 2017. Furthermore, Wall Street consensus estimates (provided by Yahoo! Finance) suggest that C could grow its revenues to $28.9 billion during 2026, which would put its stock at a Forward P/S ratio of just 1.7.

se ps ratio by data YCharts.

This means C stock would have to rise nearly 400% by the end of 2026 to trade in line with its long-term average P/S ratio of 8.7. I’m not suggesting that will happen, but I think there’s clearly scope for profit here.

Finally, another reason I invest in C is its incredibly strong balance sheet. The company ended 2025 with $11.1 billion in cash and equivalents, while only $510 million of debt, so it has a fair amount of resources. C’s cash position is improving due to rising profits, so there is nothing stopping the management from investing aggressively in growth from here.