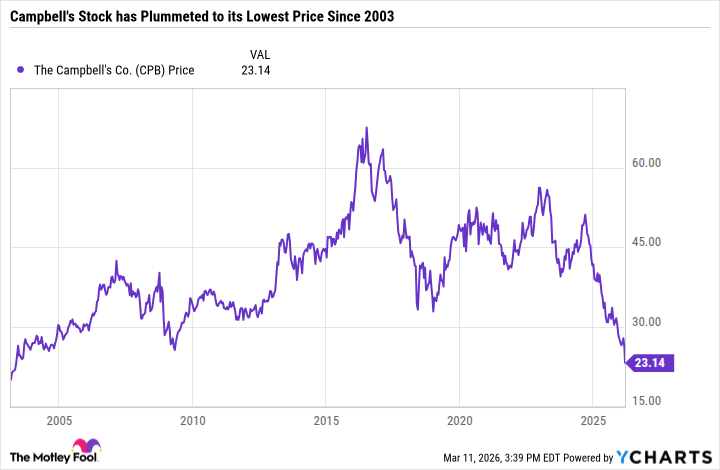

shares of campbell (cpb +0.80%) The stock fell to a 23-year low on March 11 in response to disappointing quarterly earnings results and guidance cuts. With so many going wrong, it may seem counterintuitive to go ahead and buy stocks. But Campbell is shaping up to be a compelling high yield dividend stocks For ultra-long-term value investors. here’s why.

Image Source: Getty Images.

from bad to worse

When Campbell announced its fiscal 2026 first-quarter results in December for the three months ending November 2, 2025 – the food and beverage company guided for full-year organic net sales growth of negative 1% to positive 1% and adjusted earnings per share (EPS) for a range of 12% to 18%. But in Campbell’s latest quarterly earnings for the period ending February 1, 2026, the company updated its forecast – projecting a 1%-2% decline in net sales and 23%-26% lower adjusted EPS to a new range of $2.15 to $2.25.

Stressed consumer spending is weighing heavily on Campbell’s results. But consumer pressures could now get even worse, given that Campbell’s latest quarterly results did not reflect the impact of inflation. rising oil prices From the beginning of February.

on March 11 earnings callDespite Goldfish’s strength, management attributed the snack segment’s weak performance to its fresh bakery and salty snack product lines as the main drivers. But other than promotions and pricing adjustments, there’s little hope this segment will change any time soon.

The good news is that the food and beverages segment is holding up quite well, with good margins due to growth in aspects of Rao’s Tomato Sauce and Soup segment, which focuses on cooking ingredients rather than stand-alone meal replacements.

Campbell’s is good value and can afford its dividend

In addition to cutting its guidance, Campbell reduced its full-year capital spending by $50 million and suspended its stock repurchase program to improve cash flow and address its debt load. It also said it would not raise its dividend in the near future, although it remained committed to the payment.

Campbell has not cut its dividend since 2001. Full-year guidance of $2.15 to $2.25 in adjusted EPS is still enough to cover Campbell’s annual dividend of $1.56 — though the margin for error is shrinking. But given that Campbell’s yield is at an all-time high of 6.9%, it will still be in high-yield territory even if it cuts its dividend by a third or half.

Based on the stock price at the time of this writing and the midpoint of revised earnings guidance of $2.20 per share, Campbell trades at just 10.5x earnings, which is very cheap. Granted, if this happens, Campbell’s valuation could fall further. The basics are getting worse.

today’s change

(0.80%) $0.17

current price

$21.56

key data points

market cap

$6.4B

day limit

$21.38 -$21.81

52wk range

$21.19 -$40.59

volume

303K

average volume

7.7M

gross margin

29.23%

dividend yield

7.23%

A deeply value stock for patient investors

Campbell is worth buying because it can still afford its dividend, stock is cheapAnd its portfolio of brands is better than the market is giving it credit for today.

Some investors may prefer to wait to buy Campbell until it shows signs that the worst of its recession is over. But risk-tolerant investors may want to go ahead and buy dividend stock Now, given the compelling valuation and passive-income opportunity.