© Puttachat Kumkrong / Shutterstock.com

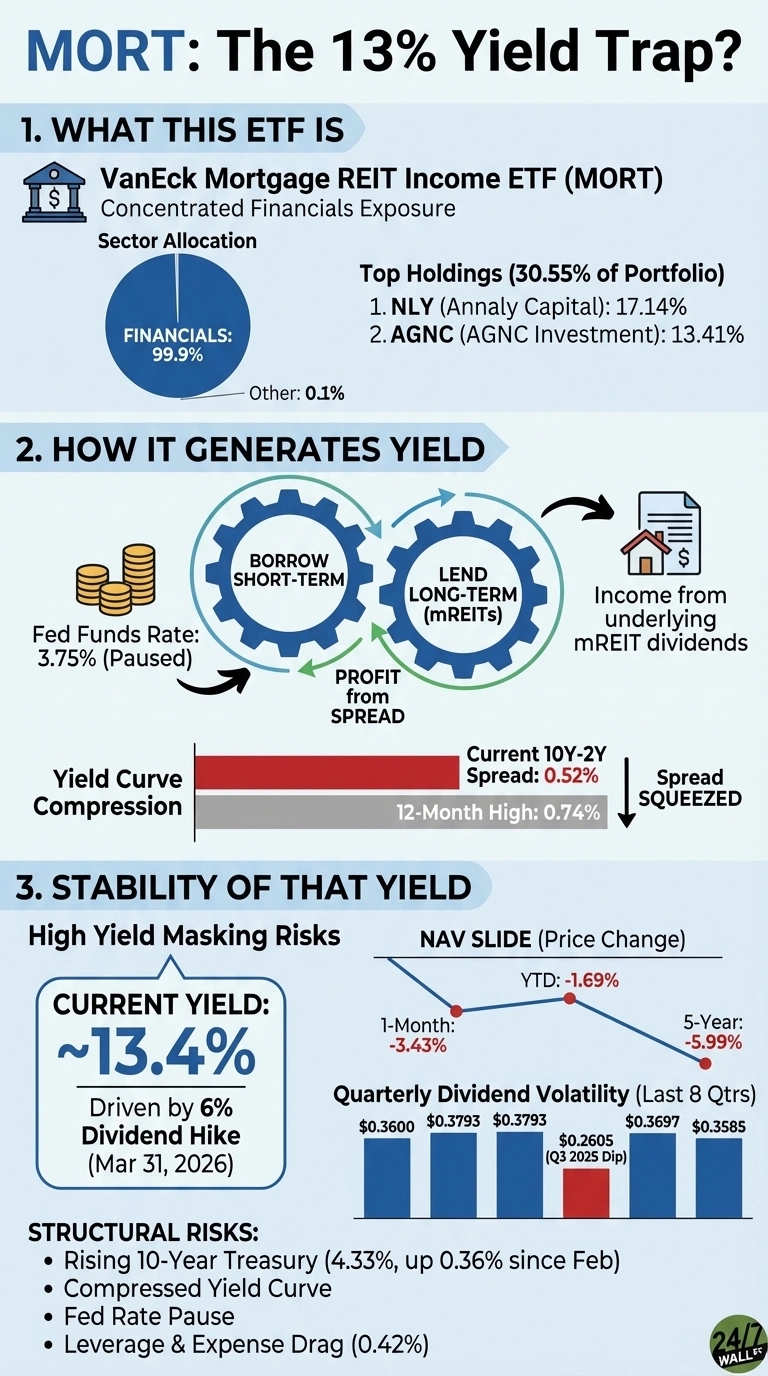

VanEck Mortgage REIT Income ETF (NYSEARCA: Mort) announced a ~6% dividend hike to March 31, 2026, taking its trailing yield to a level that attracts the attention of income-oriented investors across the market. The yield is now near 13.4% with MORT covered-call etf and leveraged bond funds as one of the highest-yield vehicles available to retail investors. The underlying holdings tell a more diverse story.

How does MORT generate its income

MORT has shares mortgage real estate investment trustCompanies that borrow at short-term rates and invest in mortgage-backed securities or originate real estate loans. The income distributed by MORT comes from dividends paid by the underlying mREITs to their shareholders.

mREIT income depends almost entirely on the difference between borrowing costs and lending yield. When short-term rates are low and long-term mortgage rates are high, the spread is wide and profitable. When that gap narrows, or rising rates destroy existing mortgage portfolios, book values fall, and dividends come under pressure.

The portfolio is almost entirely concentrated in real estate, comprising 100% of the assets. The top two holdings, Annaly Capital Management with 17.47% and AGNC Investments with 14.12%, together represent 31.59% of the fund. The top five holdings account for just over 50% of the portfolio. What happens to those two companies will largely determine what happens to MORT’s distribution.

Rate Environment Is Squeezing Out Propagation

The 10-year Treasury yield is currently at 4.31%, up 0.36% from a low of 3.96% in just over a month in late February.

The Federal Reserve’s target rate is 3.75% and is unchanged through December 11, 2025. This pause matters because mREITs borrow at rates tied to short-term benchmarks. The 10-year minus 2-year Treasury spread, which measures the profitability of the lend-short, lend-long model, is currently at 0.52%, just below its 12-month high of 0.74% in January 2026. This compression directly squeezes the net interest margin that funds MORT’s distributions.

What do the top holdings show?

Annaly reported earnings available for distribution in the fourth quarter of 2025 of $0.74 per share and declared a common stock cash dividend of $0.70 per share for the quarter. The company’s portfolio reached $104.7 billion in Q4, and CEO David Finkelstein pegged 2025 for delivery. “20% economic returns and 40% total shareholder returns.” In themselves, Annaly’s recent results look solid.

The AGNC picture is more uneven. The company reported Q4 2025 earnings of $0.83 per share and a total stock return of 34.8% with dividends reinvested for the full year. But Q2 2025 told a different story: AGNC recorded a net loss of $0.17 per share as spreads on agency MBS increased after the Liberation Day tariff announcement, causing the real book value to fall 5.3% to $7.81 per share. That quarter demonstrated how quickly mREIT book values can deteriorate when the market takes re-pricing risks.

AGNC pays a monthly common dividend of $0.12 per share. Its current share price is near $10, which is down about 2% year to date and down about 7% over the past month. Annaly is trading near $21, down about 1% year to date and down about 4% in the past month.

NAV slides behind yield headline

MORT’s market price reflects the same underlying tensions. Currently trading near $10, the ETF has slipped about 5.2% since January and 3% in the past month, giving the 5-year price a decline of about 6%. This highlights the primary risk for income investors: the danger that NAV erosion could significantly offset or neutralize the high distribution yield.

The fund’s quarterly payouts have seen significant variation recently, fluctuating between $0.2502 and $0.3793 over the past eight quarters. This volatility dropped to $0.2605 at the end of 2025, after which there was a slight rally. While the current double-digit yield appears attractive against the low share price, it’s important to note that the full dollar payout is well below the $0.42 to $0.64 range seen prior to 2020.

structural risk

- Rate Trajectory: The net interest margin for mREITs generally increases when short-term borrowing costs fall or the yield curve rises. Currently, with the Fed pausing its rate-cutting cycle at 3.75% and 10-year yields rising since late February, the environment for spread expansion remains constrained.

- Leverage Concentration: High leverage acts as a double-edged sword for book value. AGNC closed 2025 with a portfolio of $94.8 billion, supported by approximately $12.4 billion of equity, while Annaly reported a GAAP leverage ratio of 7.2x in Q4. These levels also amplify the impact of minor fluctuations in mortgage-backed security (MBS) pricing.

- Declaration Pattern: Signaling is transferred from MORT’s board; The fund moved from the December 2024 announcement, which locked in all 2025 payments, to a more conservative January 2026 approach covering only the immediate period. This shift toward shorter-horizon announcements often reflects a more defensive stance on forward-looking yield certainty.

- Drag Expenses: In addition to internal leverage and hedging costs managed by its constituent REITs, MORT charges a 0.42% net expense ratio. For investors, this creates an additional hurdle, as the ETF’s total returns must overcome this fee layer amid an already volatile income landscape.

total return reference

Over a one-year horizon, MORT’s value return is approximately -1.1%, yet the inclusion of the hefty quarterly distributions yields a positive total return for shareholders. Conversely, the five-year price decline of nearly 6% serves as a stark reminder: Investors who invested during the recent tightening cycle suffered significant NAV erosion, which substantially reduced the benefits of those high-yield payouts.

What does yield actually represent?

While the recent dividend increase is a solid increase, the 13.4% yield is largely a byproduct of the share price having fallen in line with the fund’s underlying book value. Near-term stability appears supported, as Primary Holdings Annaly and AGNC both successfully covered their recent dividends with distributable income.

However, the macro environment remains challenging; With the Federal Reserve halting its rate cut cycle and the 10-year yield rising sharply, the net interest margin required to maintain these distributions is under new pressure. Ultimately, MORT offers high-income exposure at the expense of capital preservation, as its NAV is inherently tied to interest rate volatility.