© Ilyas Nasrullah / Shutterstock.com

My order history shows another purchase realty income (NYSE:O | o price prediction) last month, and I already know the next paycheck will fund another one. I keep coming back to this stock because it pays me every month, extends that payment on a schedule I can almost set my clock to, and treats the monthly dividends as a real product.

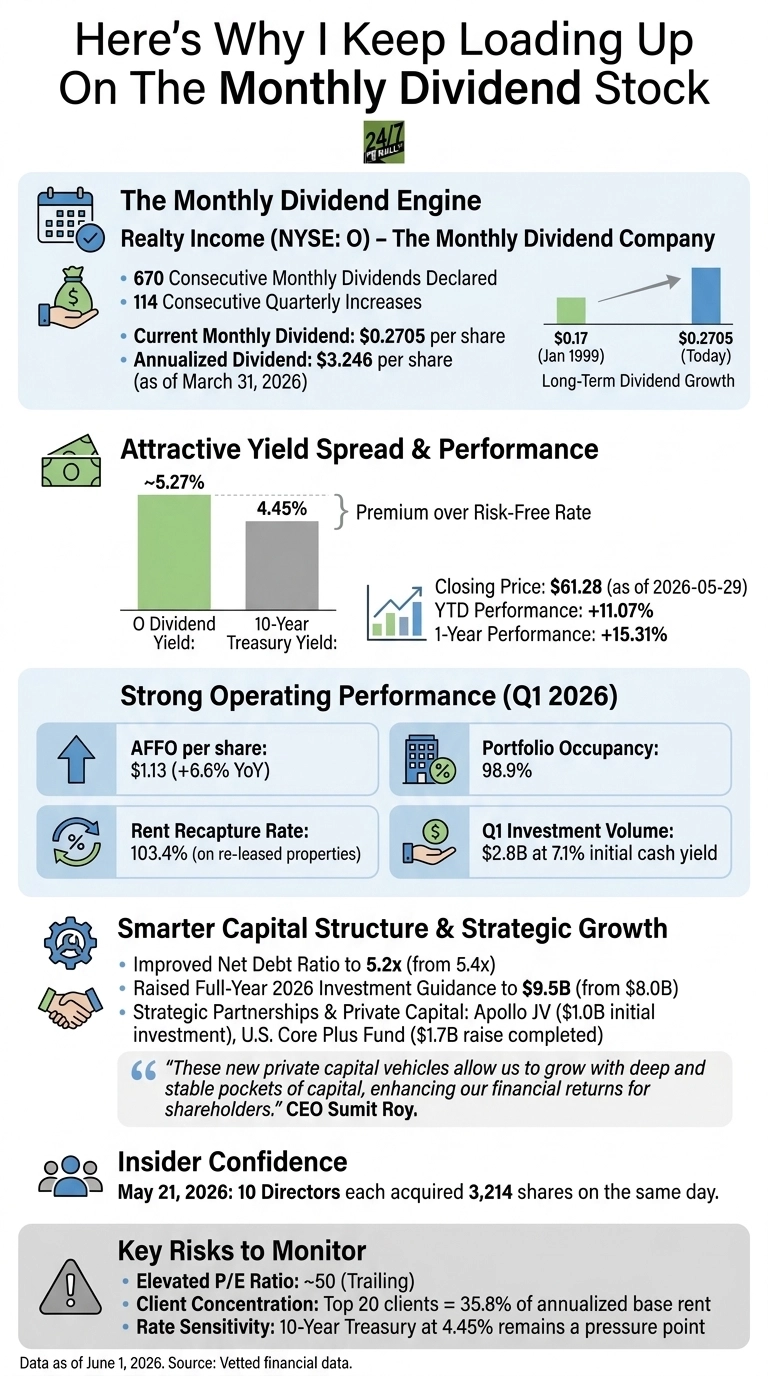

The pitch I make for myself is simple. I have a piece about a global landlord that collects rent from single-tenant commercial properties, sending checks on the 15th of the month, and the company has done this for 670 consecutive months. That rhythm matches how bills accrue in retirement. Monthly cash in account is the whole reason I started this post and is the reason I keep joining.

a reliable yield

The first data point that keeps the buy button hot is the spread. Shares closed at $61.28 with a dividend yield around 5.27%, while the 10-year Treasury was at 4.45%.

I am being paid a real premium by a company in excess of the risk-free rate Dividend raised for 114 consecutive quarters And the monthly check increased from $0.17 in January 1999 to $0.2705 today. The stock is also up 11.07% year to date and 15.31% over the last year, so income has not come at the cost of capital.

impressive basics

Second, the operating engine is expanding. In the first quarter of 2026, AFFO per share reached $1.13, up 6.6% year over year. The portfolio is 98.9% occupied, and CEO Sumit Roy is recapturing 103.4% of the pre-rent on the re-leased space.

The company invested $2.8 billion in the quarter at a 7.1% initial weighted average cash yield and raised full-year investment guidance to $9.5 billion from $8 billion. AFFO guidance increased from $4.41 to $4.44 per share. This is a landlord deploying capital at a yield higher than the cost of the loan and asking shareholders to expect more.

multiple funding lanes

Third, capital structure is becoming smarter. Net debt increased annualized pro forma adjusted EBITD to 5.2x from 5.4x. Roy stood up $1 billion joint venture with Apollo A $1.7 billion fundraise was laid for the US Core Plus fund, across 492 retail assets, and third-party private capital AUM was increased to $3.1 billion.

As Roy said, “These new private capital vehicles allow us to grow with deep and stable pockets of capital, thereby enhancing our financial returns to shareholders.” There are now more funding lanes behind dividends.

The risk I respect is concentration and rate sensitivity. The trailing P/E is near 50, the top 20 customers represent 35.8% of annual base rents, and full-year 2025 loss provisions reached $471.3 million. 10-year Treasury at 4.45% puts relative-yield pressure on each REIT.

I’m sitting with that risk because the company is still acquiring real estate at a 7.1% cash yield, the portfolio is 98.9% leased, and the dividend has increased during 2008, 2020, and every rate cycle since its NYSE listing.

Another receipt for file: On May 21, 2026, each of the ten directors acquired 3,214 shares in a single day. The people who see the fares roll in first are aligning their stock to the same month I’m buying my stock. I will Keep clicking buy As long as that check shows up on the 15th.