© kate_sept2004 / E+ via Getty Images

Northwestern Mutual’s 2025 Planning and Progress Study finds that nearly half of American millionaires (49%) say their financial planning needs improvement, and only 36% describe themselves as wealthy. People who have reached seven are reevaluating their plans and finding them inadequate. Reality: If a million dollars doesn’t seem like enough, the rest of the country has every right to ask what “on track” really means in 2026.

confidence interval

Northwestern Mutual’s data describes the people who saved, invested, and did the math themselves. What’s great is that 79% of American millionaires report their net worth as self-made, while only 12% inherited it and 5% received it unexpectedly. Roughly one in two still consider their planning inadequate, a gap between net worth and confidence.

Part of that difference stems from advisor use: 74% of millionaires work with a financial advisor, double the rate of 34% among the general population, and those with advisors feel significantly more secure and expect to retire two years earlier. Two years of retirement is a real number, which suggests that the “needs improvement” decision reflects a habit of constantly stress-testing a plan against the surrounding world rather than regret.

external environment

The world around these plans isn’t particularly cool, and this backdrop shapes how even high-net-worth families interpret their readiness. Inflation continues to be a source of unease. The Consumer Price Index reached 330.213 in April 2026, near the top of its 12-month range, indicating that price pressures have not completely subsided. Core PCE, the Federal Reserve’s preferred measure of underlying inflation, recorded 129.28 in the same month and also remained near the upper end of its recent range.

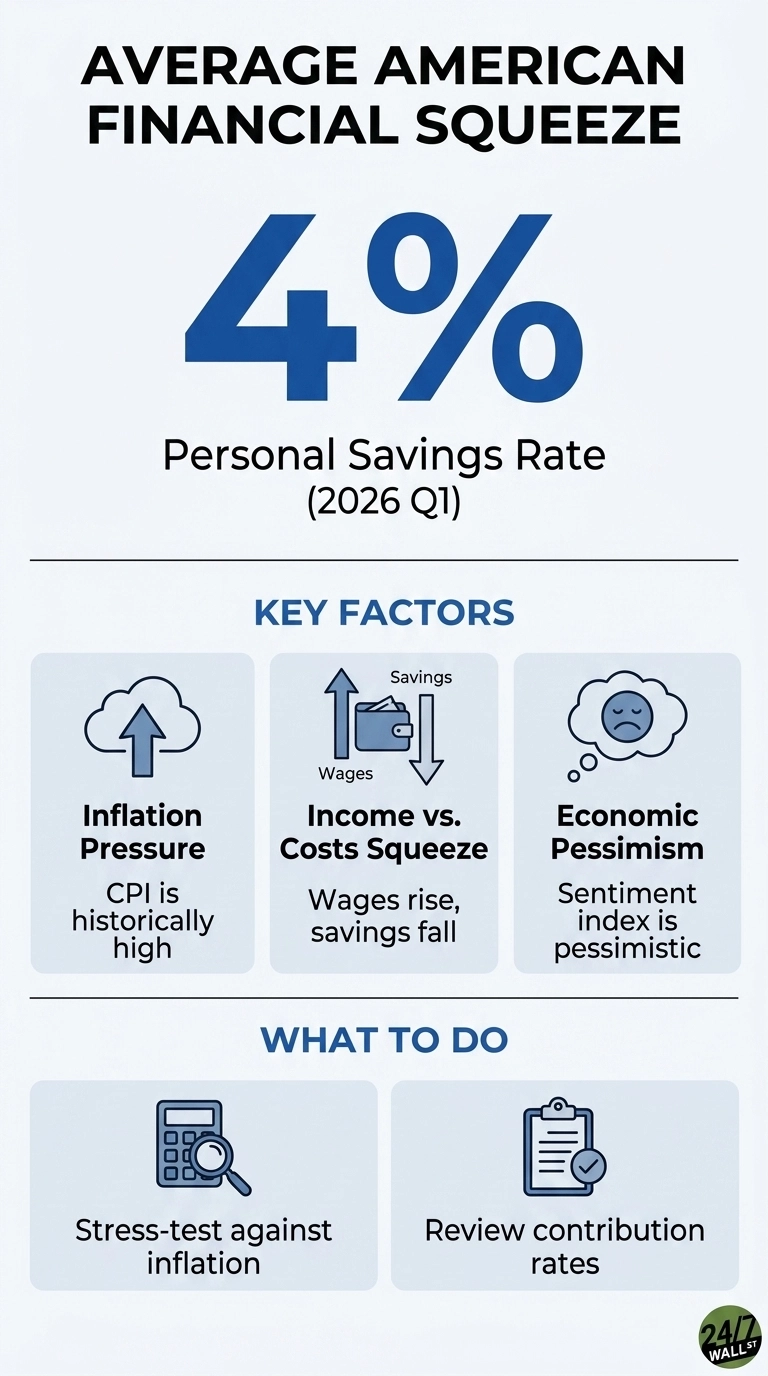

as well as, The Fed has lowered its target rate There is an increase of 0.75% compared to last year and it has been kept at 3.75% from December 11, 2025. This combination favors borrowers and reduces the returns available to savers, forcing households to re-think the assumptions made during a period when more payments are made in cash and short-term instruments. In an environment where prices remain stagnant and income from safe assets decline, even well-built plans feel the need for another round of stress testing.

Reality of cost of living

Location shapes what a million dollars can actually do, and the difference is so large that it affects how people assess their financial readiness. The cost of housing, taxes, and everyday living is higher in some parts of the country, while the same dollar costs much more in other parts. A seven-figure portfolio in a coastal metro supports a very different lifestyle than the same balance in a lower-cost area. The Bureau of Economic Analysis tracks these variations through regional price indices, and the spread across states and cities is so wide that any honest fiscal plan must account for it. Purchasing power is not a single national number. This is a local experience that changes the way families understand what “enough” really means.

comprehensive home picture

For everyone outside the millionaire class, the numbers are stark. Per capita disposable personal income was $68,617 in the first quarter of 2026, and the personal savings rate fell from 6.2% to 4% in the first quarter of 2024. On the positive side, wages continue to rise, with average hourly earnings reaching $37.41 in April 2026, up from $36.12 a year earlier, and $34.76 in April 2024. The job market is stable, with unemployment at 4.3% in April 2026. The downside is that households are saving only a tiny slice of their big paychecks, a textbook sign that cost-of-living pressures are absorbing growth.

Inheritance priorities change

The rich are rethinking what happens next. Only 53% of millionaires expect to leave an inheritance or charitable gift, and of those who do, only 12% identify leaving something for the next generation as their most important financial goal. The classic image of a millionaire accumulating wealth for grandchildren is fading as needs shift toward funding a long retirement, hedging against inflation and covering health care costs, pushing inheritance out of the top priority.

Reference to data

If 49% of self-made millionaires think their plan needs to work in an environment of inflation expectations, falling rates and rising wages, the relevant question for everyone else is what their own plan is designed to do. Northwestern Mutual data documents a mood, not a decision. Reviewing contribution rates, stress-testing retirement numbers against today’s inflation readings, and writing down what a plan should do are steps millionaires in the survey are taking. The million-dollar mark doesn’t eliminate homework.